July 13, 2026

In brief

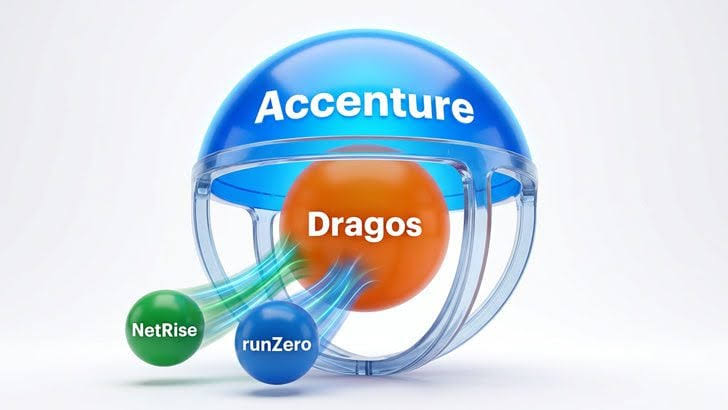

Dale Peterson argues that the Accenture–Dragos deal significantly widens the gap between Dragos and other major OT security companies. He says Dragos’ valuation is now far above Claroty and Nozomi, especially when runZero and NetRise are included, and he treats Nozomi’s Mitsubishi Electric acquisition as the clearest comparison point. He also notes that the higher Dragos valuation may help Claroty, because Claroty would likely need a valuation closer to Dragos than Nozomi for a sale or IPO to make sense.

The broader market impact, in Peterson’s view, is mostly positive: the deal validates OT security as a serious investment category, may encourage funding for the next generation of OT-focused products and services, and strengthens the need for companies to explain why an IT security product is not enough for OT environments. At the same time, he believes competitors will still have room to position themselves as the “not Dragos” option, especially if customers have concerns about Dragos, its culture, or its expanding platform strategy. He also expects some integrators and consultants to hesitate before leading with Dragos, because doing so could open the door to Accenture as a competitor.

Source: Dale Peterson – ICS Security Catalyst